[ad_1]

Share prices of Micron Technology (NASDAQ: MU) took off big time following the company’s fiscal 2024 second-quarter results (for the three months ended Feb. 29), which were released on March 20. The stock rose over 14% in a single session thanks to outstanding growth in revenue and earnings. Micron’s metrics crushed Wall Street expectations, and its guidance was strong enough to confirm the company’s turnaround has finally arrived.

Over the past year, Micron stock is up 93%. Management’s projections for future revenue growth (see below) suggest this stock might just have more upside left in the tank. Let’s look at the numbers and see why investors should consider buying this chipmaker before its next set of elevated revenue projections reach their target dates.

Micron has stepped on the gas

In this most recent quarter, revenue shot up 58% year over year to $5.82 billion. That was well ahead of the $5.35 billion consensus estimate. Even better, Micron swung to an adjusted profit of $0.42 per share from a loss of $1.91 per share in the year-ago period. Analysts were expecting a loss of $0.25 per share last quarter.

A favorable supply-demand balance in the memory-chip market meant that prices headed higher last quarter, allowing Micron to significantly boost its margins. Management said that the prices of dynamic random-access memory (DRAM) shot up in the high teens last quarter, while the price of NAND flash storage chips was up 30%.

All this explains why the company’s adjusted gross margin increased to 20% in the previous quarter as compared to a negative 31.4% in the year-ago period. And an operating margin of 3.5% was a massive improvement compared to the negative 56% in the prior-year period.

CEO Sanjay Mehrotra credited the growing memory demand for artificial intelligence (AI) servers as a key reason behind its turnaround. He said on the latest earnings conference call:

This improvement in market conditions was due to a confluence of factors, including strong [artificial intelligence (AI)] server demand, a healthier demand environment in most end markets, and supply reductions across the industry. AI server demand is driving rapid growth in HBM [high-bandwidth memory], DDR5 [D5] and data center SSDs, which is tightening leading-edge supply availability for DRAM and NAND.

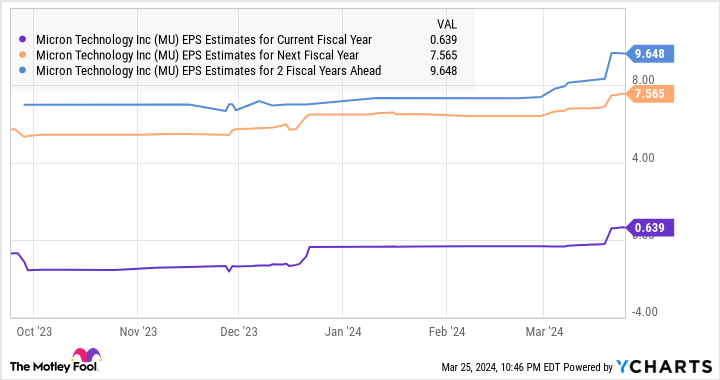

Mehrotra expects memory prices to head higher as the year progresses and forecasts Micron will generate “record revenue and much-improved profitability now in fiscal year 2025.” The company’s outlook for the current quarter turned out to be well ahead of what analysts were expecting.

Micron expects fiscal 2024 third-quarter revenue of $6.6 billion and adjusted earnings of $0.45 per share at the midpoint of its guidance range. Wall Street was looking for just $0.09 per share in earnings on revenue of $6 billion. Year over year, revenue is on track to increase by 76%, which would be a nice improvement over the growth the company posted last quarter.

Micron recorded a loss of $1.19 per share in the same period last year, which means that the recovery in memory prices is all set to give its bottom line a big boost. This helps explain why analysts are raising their bottom-line growth expectations following Micron’s latest report.

Buying the stock is a no-brainer move

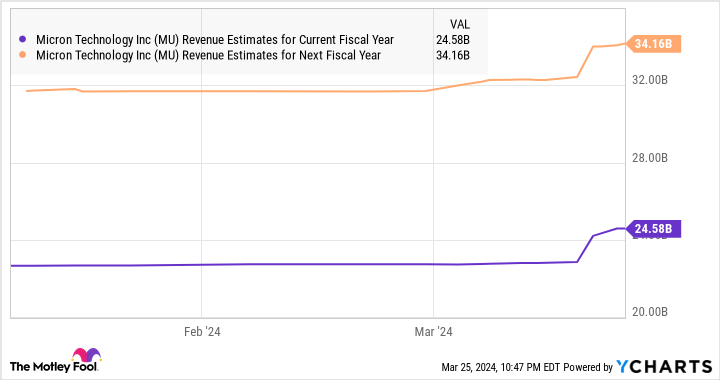

Micron stock trades at 6.4 times sales, lower than the U.S. technology sector’s price-to-sales ratio of 7.3. According to consensus estimates, Micron could end the current fiscal year with $24.6 billion in revenue. That would be a 58% jump from last year. And it is expected to sustain an impressive growth rate next year as well.

Assuming Micron does hit $34 billion in revenue in fiscal 2025 and maintains its current price-to-sales ratio, its market cap could jump to $217 billion. That would be a 67% jump from current levels. So investors are getting a good deal on Micron stock right now, making it a good idea to buy it before it soars further following its latest earnings report.

Should you invest $1,000 in Micron Technology right now?

Before you buy stock in Micron Technology, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Micron Technology wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 25, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

1 Incredible Growth Stock to Buy Before Its Market Cap Jumps 67% was originally published by The Motley Fool

[ad_2]